Situation of the French semiconductor market at 3rd quarter 2024

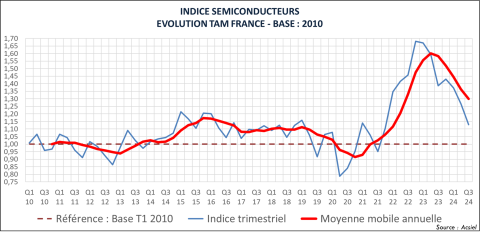

Paris, December 4, 2024 – The French semiconductor market contracted by 11% in the third quarter compared with the previous quarter, to €486 million, according to Acsiel Alliance Electronique. Year-on-year, the market is down 19% (compared to third-quarter 2023). The French market index on a sliding annual average has been declining for five quarters (see graph below).

The main contributor to the market downturn was distribution, with a quarter-on-quarter drop of 27% (or -36% year-on-year). The distribution channel, which represented 39% of the total market in the second quarter, accounted for only 32% in the third.

Direct sales were virtually stable (-0.6% to €332 million). However, there were wide disparities between segments. Sales to the industrial segment fell by 47%, so that their share of direct sales dropped from 29% to 16% quarter-on-quarter. By contrast, all other segments enjoyed growth of 19%. The main contribution to this growth came from the automotive sector (+16%). Defense/Aerospace rebounded with +33% after two negative quarters, as did Smart Card (+11%). In terms of direct sales by product family, the rebound of analog circuits (+32%) and microcontrollers and microprocessors (+10%) clearly pulled the market upwards. Conversely, MOS logic circuits, at -18%, experienced their third consecutive quarter of sharp decline.

In a market that remains generally on a downward trend, some positive trends are emerging. The automotive segment is showing signs of recovery, with billings at their highest level since the all-time record set in the first quarter of 2023. Smart card sales are proving resilient. The Defense/Aeronautics/Space sector confirms its good momentum, being the only one to record year-on-year growth over the first three quarters (+7%). Although IT accounts for a small share of the French market, it is nonetheless in a position to benefit from the growth of data centers in terms of energy management.

Although the French market is still penalized by inventory corrections, these are about to come to an end. According to Acsiel, the industrial segment was the main contributor to the market downturn in the third quarter, and this goes a long way towards explaining the underperformance of distribution sales, of which industrial accounts for more than two-thirds. Among the multiple sectors that make up the industrial segment, it is possible to identify causes of weak demand in France, such as the slump in the construction industry or the delay in the installation of charging stations for electric vehicles. More broadly, Chinese competition with our customers for finished products (energy, industrial equipment) is becoming increasingly pressing, as well as for certain electronic components.

The slowdown in the French market can also be attributed to a wait-and-see attitude due to the political and economic context, which is delaying certain projects. At the same time, the semiconductor industry has made huge investments to better meet demand, which has already led to a reduction in delivery times, putting it in a favorable position to react to the market upturn.

Quarterly trends in the French market since 2010, in indexes, annual moving average – Source ACSIEL